A hailstorm can be over in minutes. The damage it leaves behind can linger for months. Few things frustrate homeowners more than opening a letter from their insurance company and discovering that their claim has been denied. If you are searching for What to Do If Your Hail Claim Was Denied in La Porte, TX, you are not alone. Every year, property owners across Texas receive denial notices after severe weather events, even when they believe legitimate damage exists. The good news? A denied claim does not automatically mean the process is over.

Many hail claims are successfully reopened, reconsidered, or resolved after additional evidence is presented. In some cases, homeowners discover that important damage was overlooked during the original inspection. In others, the insurer simply lacked sufficient documentation to support payment. The key is knowing what to do next. This guide explains the practical steps homeowners can take after a denial, how to strengthen their position, and how to pursue a fair outcome when hail damage affects their property in La Porte, TX.

Understanding Why Hail Claims Get Denied

Before taking action, it helps to understand why insurance companies deny hail claims in the first place. Not every denial is caused by bad faith or unfair treatment. Sometimes there is a legitimate disagreement about what caused the damage. Other times, the insurer simply does not have enough evidence to justify payment. Understanding the reason behind the denial helps determine the best path forward.

Common Reasons Hail Claims Are Denied

Several issues appear repeatedly in denied hail claims.

Lack of Visible Hail Damage

An adjuster may inspect the property and conclude that hail did not cause the observed conditions. This frequently happens when impacts are subtle or difficult to identify.

Wear and Tear

Insurance policies generally cover sudden storm damage, not gradual deterioration. If an insurer believes roof conditions developed over time rather than during a hailstorm, a denial may follow.

Pre-Existing Damage

Older roof problems often become part of claim disputes. The carrier may argue that damage existed before the reported storm.

Late Reporting

Waiting too long to report hail damage can create challenges. The longer the delay, the harder it becomes to establish when damage occurred.

Policy Exclusions

Some policies contain limitations involving cosmetic damage, older roofing systems, or specific materials.

Why Denials Happen More Often Than Homeowners Expect

Many people assume that visible roof damage automatically results in coverage. Unfortunately, insurance claims are not always that straightforward.

Adjusters evaluate:

- Cause of damage

- Extent of damage

- Policy language

- Maintenance history

- Inspection findings

- Weather records

When any of those elements create uncertainty, disputes can arise. That is why the first step after a denial is understanding exactly why the claim was rejected.

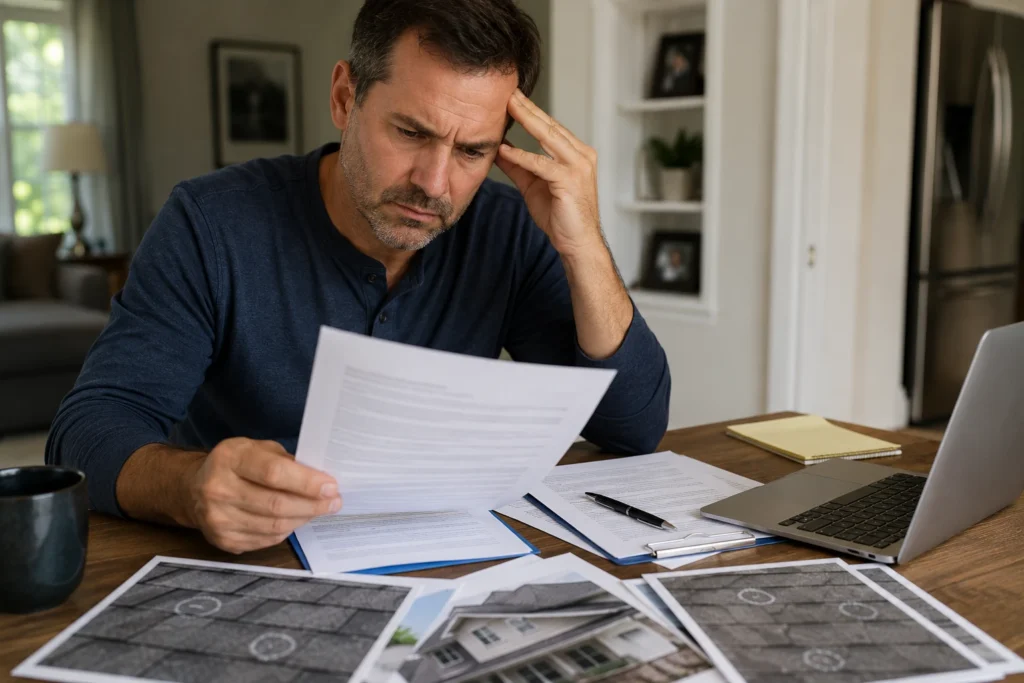

Step One: Carefully Review the Denial Letter

This sounds obvious. Yet many homeowners skim the denial letter, become frustrated, and immediately start arguing with the insurance company without fully understanding the carrier’s position. Slow down. Read every word. The denial letter often contains valuable clues that help shape your response.

Key Information to Look For

Review the letter for:

| Item | Why It Matters |

|---|---|

| Reason for denial | Identifies the insurer’s position |

| Policy references | Shows what coverage language was used |

| Inspection findings | Explains what the adjuster observed |

| Exclusions cited | Reveals policy limitations |

| Appeal information | Outlines next steps |

Pay close attention to exact wording.

For example, there is a major difference between:

- “No hail damage was observed.”

- “Damage was observed but is not covered.”

One challenges the existence of damage. The other challenges coverage. Those require very different responses.

Watch for Vague Explanations

A denial letter should clearly explain the insurer’s reasoning. If the explanation feels incomplete or confusing, that may indicate the need for additional investigation.

Examples include statements such as:

- “Damage appears unrelated to the storm.”

- “Claim does not qualify for payment.”

- “Observed conditions are excluded.”

Those conclusions should be supported by evidence. If they are not, further review may be warranted.

Step Two: Review Your Insurance Policy

The next step is understanding your coverage. Many homeowners never read their policy until a claim is denied. That is understandable. Insurance contracts are not exactly light reading. Still, policy language matters. A lot.

Focus on These Sections

Review:

- Dwelling coverage

- Wind and hail coverage

- Roof endorsements

- Exclusions

- Deductibles

- Conditions and duties after loss

Understanding these provisions helps determine whether the denial aligns with the actual contract.

Why Policy Language Can Be Critical

Two homeowners on the same street may experience identical hail damage and receive different claim outcomes. Why? Different policies. Different endorsements. Different exclusions. The insurer’s obligations depend on the exact wording contained within the policy. This is where attention to detail becomes extremely important.

Step Three: Gather Independent Evidence

A denial should never end your investigation. In many cases, it should start one. The strongest responses to denied claims rely on evidence rather than emotion. The goal is simple. Document everything.

Schedule an Independent Roof Inspection

An experienced roofing professional can provide a second opinion regarding storm-related damage. Independent inspections often identify issues that were overlooked during the initial evaluation.

Examples include:

- Hail bruising

- Granule loss

- Impact fractures

- Damaged flashing

- Vent damage

- Ridge cap damage

The inspection should include photographs whenever possible. Visual evidence often carries significant weight.

Document Every Affected Area

Roofs receive the most attention after hailstorms. However, damage can extend far beyond roofing materials.

Inspect:

- Gutters

- Downspouts

- Siding

- Window screens

- Air conditioning units

- Fences

- Outdoor equipment

Each damaged component helps establish the severity of the storm.

Collect Supporting Documentation

Strong claim files usually include:

- Photographs

- Videos

- Contractor reports

- Inspection findings

- Maintenance records

- Repair estimates

Organization matters. The easier it is to present evidence, the easier it becomes for decision-makers to evaluate your position.

Weather Data Can Strengthen Your Case

One overlooked tool involves storm verification. Weather reports can help demonstrate that hail occurred near your property on the date of loss. Many professionals use storm tracking information to support claim documentation. Interestingly, modern weather analysis often relies on sophisticated mathematical modeling techniques similar to concepts studied in Topology, where complex systems are analyzed through structural relationships and patterns. While homeowners do not need advanced mathematics, they do need credible storm evidence.

Helpful documentation may include:

- Hail reports

- Radar data

- National Weather Service records

- Local storm reports

When combined with physical damage evidence, weather data can strengthen a denied claim significantly.

Step Four: Learn How to Document Hail Damage for an Insurance Claim

One of the biggest mistakes homeowners make is taking too few photographs. Another common mistake? Taking poor photographs. Insurance companies make decisions based on evidence. The better your documentation, the stronger your position becomes.

Photograph Damage Correctly

Take photographs from multiple angles.

Capture:

- Close-up damage

- Wide-angle views

- Entire roof sections

- Individual impacts

- Surrounding property damage

Good lighting matters. So does image quality. Avoid blurry photographs whenever possible.

Create a Damage Timeline

A timeline can help establish the sequence of events.

Document:

| Event | Date |

|---|---|

| Storm occurrence | Date of storm |

| Damage discovery | Date found |

| Claim reported | Date filed |

| Inspection completed | Date inspected |

| Denial received | Date denied |

Timelines often help clarify disputes involving reporting delays.

Save Everything

Do not discard:

- Letters

- Emails

- Estimates

- Inspection reports

- Photographs

- Text messages

If the dispute escalates later, these records may become extremely valuable.

Request a Reinspection

Once you have gathered additional evidence, a reinspection may be appropriate. Many denied claims are revisited after new information becomes available. A reinspection provides another opportunity for the insurer to evaluate the damage.

Situations That Often Justify a Reinspection

Consider requesting another inspection if:

- New damage evidence exists

- A contractor identified overlooked damage

- Additional storm documentation was obtained

- Initial inspections were limited

The goal is not confrontation. The goal is accuracy. A well-prepared reinspection request supported by evidence often produces better results than an emotional complaint.

Prepare Before the Adjuster Arrives

Do not wait until the day of the inspection. Prepare in advance.

Create a package containing:

- Damage photos

- Contractor findings

- Repair estimates

- Weather documentation

- Maintenance records

Present information clearly and professionally. Remember, decision-makers evaluate evidence. The stronger the evidence, the stronger the claim.

Appealing a Denied Hail Claim

If your claim remains denied after gathering additional evidence, the next step may be a formal appeal. Many homeowners assume an appeal is simply asking the insurance company to reconsider. It is much more than that. A strong appeal presents facts, documentation, and expert findings that directly address the reasons for denial. The process should be professional and organized.

What a Strong Appeal Should Include

A well-prepared appeal package often contains:

- A written summary of the dispute

- Copies of the denial letter

- Independent inspection reports

- Photographs documenting damage

- Contractor estimates

- Weather records

- Maintenance documentation

The goal is to create a clear narrative supported by evidence. Imagine a decision-maker reviewing your file weeks or months after the storm. Would the documentation tell a convincing story? If not, continue strengthening it.

Focus on Facts

It is understandable to feel frustrated after a denial. However, emotional arguments rarely change claim outcomes. Facts do.

Instead of saying:

“The insurance company is wrong.”

Provide evidence showing why the conclusion may be incorrect. That approach is significantly more effective.

Follow Up Consistently

Appeals can take time. Stay engaged throughout the process.

Keep records of:

- Phone calls

- Emails

- Letters

- Inspection appointments

- Claim updates

Consistency often helps prevent unnecessary delays.

The Appraisal Clause: An Important Option in Texas

Many Texas homeowners are unfamiliar with one of the most powerful dispute-resolution tools available in property insurance policies. The appraisal clause. When applicable, appraisal can help resolve disagreements regarding the amount of loss.

What Is Appraisal?

Appraisal is a process where each side selects an appraiser. The two appraisers then attempt to agree on the value of the damage. If they cannot agree, an umpire may become involved. The process is designed to resolve valuation disputes without lengthy litigation.

How Appraisal Typically Works

| Step | Description |

|---|---|

| Demand for appraisal | One party invokes the clause |

| Appraiser selection | Each side chooses an appraiser |

| Damage evaluation | Appraisers inspect and assess losses |

| Umpire involvement | Used if disagreements remain |

| Final determination | Award establishes loss value |

Appraisal often moves faster than a lawsuit and may help settle significant disputes.

When Appraisal May Be Helpful

Appraisal is often useful when:

- Damage exists but value is disputed

- Repair versus replacement is disputed

- Scope of repairs is disputed

- Pricing disagreements exist

However, appraisal may not resolve every issue. Coverage disputes sometimes require different solutions. That is why understanding the reason for denial remains critical.

When Hiring a Public Adjuster Makes Sense

Some claim disputes become too complicated for homeowners to handle alone. There is no shame in seeking professional assistance. In fact, doing so can save substantial time and stress.

What a Public Adjuster Does

A public adjuster works on behalf of the policyholder rather than the insurance company.

Responsibilities often include:

- Reviewing policy language

- Inspecting damage

- Documenting losses

- Preparing estimates

- Negotiating claim settlements

Their role is to help ensure the claim is properly evaluated.

Situations Where Professional Help May Be Valuable

Consider seeking assistance if:

- The claim involves substantial damage

- Multiple inspections have occurred

- The insurer continues to dispute findings

- Documentation requirements become overwhelming

- Significant financial exposure exists

The larger the claim, the more important proper documentation becomes.

Why Local Knowledge Matters

Property owners dealing with What to Do If Your Hail Claim Was Denied in La Porte, TX often benefit from professionals familiar with local weather patterns and claim issues. La Porte properties face unique weather challenges. Storm systems moving through the Gulf Coast region can produce varying damage patterns, making accurate documentation particularly important. Local experience can sometimes help identify issues that might otherwise be overlooked.

Filing a Complaint with the Texas Department of Insurance

Sometimes disputes extend beyond damage assessments. Homeowners may believe their claim was mishandled or that communication has broken down. When that happens, filing a complaint with the Texas Department of Insurance may be appropriate.

What the Department Can Do

The Texas Department of Insurance can review:

- Claim handling concerns

- Communication issues

- Potential regulatory violations

- Complaint patterns

While the agency does not guarantee claim payment, it can help ensure insurers follow applicable rules and procedures.

Information You Should Gather

Before filing a complaint, collect:

- Policy information

- Claim number

- Denial letter

- Correspondence records

- Inspection reports

- Supporting evidence

The more organized your submission, the easier it becomes for reviewers to understand the dispute.

When a Complaint Makes Sense

Potential situations include:

- Significant communication delays

- Unclear denial explanations

- Failure to respond to inquiries

- Concerns about claim handling practices

Documentation remains essential here as well.

A complaint supported by evidence is always stronger than one supported only by frustration.

When Legal Action May Become Necessary

Most hail claim disputes never reach a courtroom. Many are resolved through documentation, negotiation, reinspection, appraisal, or settlement discussions. Occasionally, however, legal action becomes necessary.

Situations That May Require Legal Review

Examples include:

- Persistent claim denials despite strong evidence

- Significant financial losses

- Coverage disputes involving policy interpretation

- Allegations of improper claim handling

Legal counsel can help evaluate available options.

Why Documentation Becomes Even More Important

If a dispute escalates, every document matters.

Keep copies of:

- Claim submissions

- Denial letters

- Inspection reports

- Estimates

- Emails

- Photographs

- Weather documentation

Well-organized records often become one of the strongest assets in a claim dispute.

Common Mistakes That Hurt Denied Hail Claims

Many denied claims become harder to resolve because homeowners unintentionally weaken their own position. Avoid these common mistakes.

Waiting Too Long

Time matters. Delays can make evidence harder to collect and damage harder to evaluate. Act promptly whenever possible.

Throwing Away Documentation

Every document may have value later. Store everything in digital and physical formats whenever possible.

Relying Solely on Verbal Conversations

Phone calls are useful. Written records are better. Always document important conversations.

Making Repairs Before Documentation

Emergency mitigation may be necessary. However, major repairs should be documented thoroughly before work begins. Once evidence disappears, it may be difficult to reconstruct.

Assuming the First Denial Is Final

Many homeowners stop pursuing valid claims after receiving a denial. That can be a costly mistake. Insurance decisions are often reconsidered when additional evidence emerges.

A Realistic Example of a Denied Hail Claim in La Porte, TX

Imagine a homeowner in La Porte notices roofing issues after a severe storm. The claim is filed promptly. An inspection occurs. Weeks later, the insurance company denies the claim, stating that the roof damage appears related to age rather than hail. At first, the homeowner feels stuck. But instead of accepting the denial, they gather additional information.

An independent inspection identifies impact damage on roofing materials, gutters, and metal components. Weather records confirm hail activity near the property. Detailed photographs are collected. A reinspection is requested. After reviewing the new evidence, the insurer reevaluates the claim and ultimately approves portions of the loss that were previously denied. This example illustrates an important reality. Initial claim decisions are not always the final outcome. Evidence changes cases.

Preventing Future Hail Claim Problems

While no homeowner can prevent hailstorms, several proactive steps can reduce future claim challenges.

Document Your Property Before Storm Season

Create a baseline record.

Photograph:

- Roof surfaces

- Gutters

- Siding

- Windows

- Exterior structures

Having pre-storm photographs can be incredibly valuable later.

Maintain Your Property

Routine maintenance helps reduce disputes involving wear and tear allegations.

Keep records of:

- Roof inspections

- Repairs

- Maintenance work

- Contractor visits

These records can help establish the property’s condition before a storm.

Understand Your Policy Before a Loss Occurs

Many claim disputes arise because homeowners discover limitations only after damage occurs. Review coverage periodically.

Understand:

- Deductibles

- Exclusions

- Endorsements

- Reporting requirements

Knowledge today can prevent confusion tomorrow.

Report Damage Quickly

Prompt reporting strengthens claim documentation. The sooner damage is inspected, the easier it often becomes to establish cause and scope.

Stay Organized

Develop a simple system for storing:

- Policies

- Receipts

- Inspection reports

- Claim records

- Maintenance documentation

Organization pays dividends during claim disputes.

Final Thoughts

Facing a denied hail claim can feel discouraging. There is no way around that. When significant damage affects your home, the last thing you want to hear is that your claim has been rejected. Fortunately, a denial is often the beginning of the investigation not the end.

For homeowners researching What to Do If Your Hail Claim Was Denied in La Porte, TX, the most important takeaway is simple: focus on evidence. Review the denial carefully. Understand your policy. Gather independent inspections. Document every aspect of the loss. Request a reinspection when appropriate. Explore appraisal options when available. Seek professional guidance if the dispute becomes complex.

Most importantly, do not assume that the first answer is the final answer. Many successful claim resolutions begin exactly where denied claims start with a homeowner willing to investigate further, collect better evidence, and pursue a fair outcome. If your hail claim was denied in La Porte, TX, take a measured approach, stay organized, and continue building the strongest possible case. The right documentation, combined with persistence and professional support when necessary, can make a meaningful difference in the outcome of your claim.

FAQs

Yes. Many denied hail claims are reconsidered when new evidence, inspection reports, or weather data are submitted.

The timeframe depends on your policy and circumstances, so review your policy carefully and act as quickly as possible.

Yes. An independent inspection may identify hail damage that was missed or disputed during the original inspection.

Keep denial letters, photographs, inspection reports, estimates, emails, and all claim-related communications.

Yes. Weather records can help verify that hail occurred near your property on the reported date of loss.

Appraisal is a dispute-resolution process that helps determine the amount of damage when both sides disagree on the value of the loss.

Consider hiring a public adjuster when the claim is large, complex, or continues to face disputes after additional inspections.

Age alone does not automatically justify a denial, but insurers may argue that damage resulted from wear and tear rather than hail.

Yes. Prompt documentation helps preserve evidence and strengthens your ability to connect the damage to a specific storm event.

Carefully review the denial letter to understand the insurer’s reasoning before deciding on the next course of action.